Page 16 - economic report 2021

P. 16

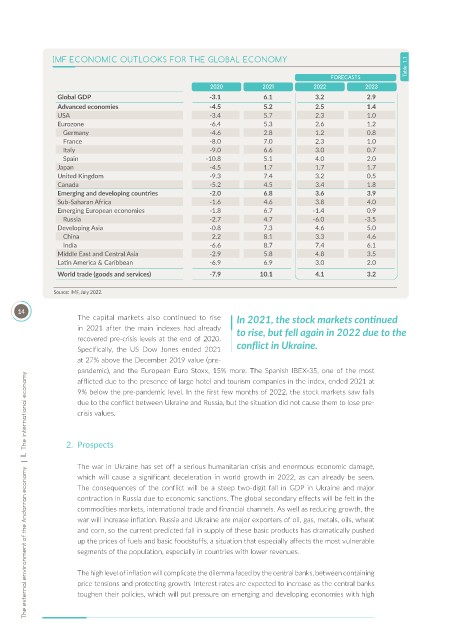

IMF ECONOMIC OUTLOOKS FOR THE GLOBAL ECONOMY

Table 1.1

FORECASTS

2020 2021 2022 2023

Global GDP -3.1 6.1 3.2 2.9

Advanced economies -4.5 5.2 2.5 1.4

USA -3.4 5.7 2.3 1.0

Eurozone -6.4 5.3 2.6 1.2

Germany -4.6 2.8 1.2 0.8

France -8.0 7.0 2.3 1.0

Italy -9.0 6.6 3.0 0.7

Spain -10.8 5.1 4.0 2.0

Japan -4.5 1.7 1.7 1.7

United Kingdom -9.3 7.4 3.2 0.5

Canada -5.2 4.5 3.4 1.8

Emerging and developing countries -2.0 6.8 3.6 3.9

Sub-Saharan Africa -1.6 4.6 3.8 4.0

Emerging European economies -1.8 6.7 -1.4 0.9

Russia -2.7 4.7 -6.0 -3.5

Developing Asia -0.8 7.3 4.6 5.0

China 2.2 8.1 3.3 4.6

India -6.6 8.7 7.4 6.1

Middle East and Central Asia -2.9 5.8 4.8 3.5

Lat n America & Caribbean -6.9 6.9 3.0 2.0

World trade (goods and services) -7.9 10.1 4.1 3.2

Source: IMF, July 2022.

14

The capital markets also continued to rise In 2021, the stock markets cont nued

in 2021 after the main indexes had already to rise, but fell again in 2022 due to the

recovered pre-crisis levels at the end of 2020.

Specifically, the US Dow Jones ended 2021 conf ict in Ukraine.

at 27% above the December 2019 value (pre-

pandemic), and the European Euro Stoxx, 15% more. The Spanish IBEX-35, one of the most

The external environment of the Andorran economy | I. The international economy

afflicted due to the presence of large hotel and tourism companies in the index, ended 2021 at

9% below the pre-pandemic level. In the first few months of 2022, the stock markets saw falls

due to the conflict between Ukraine and Russia, but the situation did not cause them to lose pre-

crisis values.

2. Prospects

The war in Ukraine has set off a serious humanitarian crisis and enormous economic damage,

which will cause a significant deceleration in world growth in 2022, as can already be seen.

The consequences of the conflict will be a steep two-digit fall in GDP in Ukraine and major

contraction in Russia due to economic sanctions. The global secondary effects will be felt in the

commodities markets, international trade and financial channels. As well as reducing growth, the

war will increase inflation. Russia and Ukraine are major exporters of oil, gas, metals, oils, wheat

and corn, so the current predicted fall in supply of these basic products has dramatically pushed

up the prices of fuels and basic foodstuffs, a situation that especially affects the most vulnerable

segments of the population, especially in countries with lower revenues.

The high level of inflation will complicate the dilemma faced by the central banks, between containing

price tensions and protecting growth. Interest rates are expected to increase as the central banks

toughen their policies, which will put pressure on emerging and developing economies with high