Page 92 - economic report 2021

P. 92

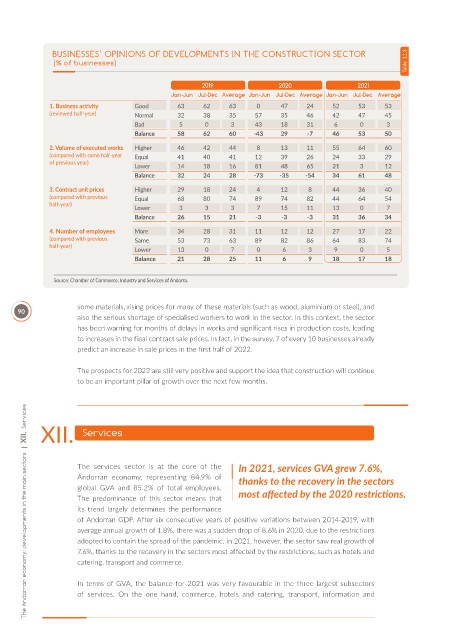

BUSINESSES’ OPINIONS OF DEVELOPMENTS IN THE CONSTRUCTION SECTOR

(% of businesses) Table 11.3

2019 2020 2021

Jan-Jun Jul-Dec Average Jan-Jun Jul-Dec Average Jan-Jun Jul-Dec Average

1. Business act vity Good 63 62 63 0 47 24 52 53 53

(reviewed half-year) Normal 32 38 35 57 35 46 42 47 45

Bad 5 0 3 43 18 31 6 0 3

Balance 58 62 60 -43 29 -7 46 53 50

2. Volume of executed works Higher 46 42 44 8 13 11 55 64 60

(compared with same half-year Equal 41 40 41 12 39 26 24 33 29

of previous year)

Lower 14 18 16 81 48 65 21 3 12

Balance 32 24 28 -73 -35 -54 34 61 48

3. Contract unit prices Higher 29 18 24 4 12 8 44 36 40

(compared with previous Equal 68 80 74 89 74 82 44 64 54

half-year)

Lower 3 3 3 7 15 11 13 0 7

Balance 26 15 21 -3 -3 -3 31 36 34

4. Number of employees More 34 28 31 11 12 12 27 17 22

(compared with previous Same 53 73 63 89 82 86 64 83 74

half-year)

Lower 13 0 7 0 6 3 9 0 5

Balance 21 28 25 11 6 9 18 17 18

Source: Chamber of Commerce, Industry and Services of Andorra.

some materials, rising prices for many of these materials (such as wood, aluminium or steel), and

90

also the serious shortage of specialised workers to work in the sector. In this context, the sector

has been warning for months of delays in works and significant rises in production costs, leading

to increases in the final contract sale prices. In fact, in the survey, 7 of every 10 businesses already

predict an increase in sale prices in the first half of 2022.

The prospects for 2022 are still very positive and support the idea that construction will continue

to be an important pillar of growth over the next few months.

The Andorran economy: developments in the main sectors | XII. Services

XII. Services

The services sector is at the core of the In 2021, services GVA grew 7.6%,

Andorran economy, representing 84.9% of thanks to the recovery in the sectors

global GVA and 85.2% of total employees.

The predominance of this sector means that most af ected by the 2020 restrict ons.

its trend largely determines the performance

of Andorran GDP. After six consecutive years of positive variations between 2014-2019, with

average annual growth of 1.8%, there was a sudden drop of 8.6% in 2020, due to the restrictions

adopted to contain the spread of the pandemic. In 2021, however, the sector saw real growth of

7.6%, thanks to the recovery in the sectors most affected by the restrictions, such as hotels and

catering, transport and commerce.

In terms of GVA, the balance for 2021 was very favourable in the three largest subsectors

of services. On the one hand, commerce, hotels and catering, transport, information and